Introduction

I have continued my reviews of Ocwen’s consumer relief and compliance obligations under the National Mortgage Settlement (NMS or Settlement). The following is a summary of the reports I filed with the United States District Court for the District of Columbia (the Court) on Ocwen’s progress through September 30, 2015, toward meeting its consumer relief obligations and Ocwen’s compliance with the Settlement. This report addresses Ocwen’s consumer relief and compliance on its entire portfolio, which includes both the loan portfolio acquired from the ResCap Parties and all other loans serviced by Ocwen in its mortgage loan portfolio.1

As a result of my review of the IRG’s work papers for Ocwen’s claimed consumer relief credit through September 30, 2015, I have credited Ocwen with $1,246,442,217 toward its consumer relief obligation. In total, I have credited Ocwen with $2,127,661,401 in consumer relief credit and have determined that Ocwen has exceeded its consumer relief obligations.

Testing Ocwen on its consumer relief and compliance for the first and second quarters 2015 involved my primary professional firms, secondary professional firms and other professionals. Together, these professionals dedicated approximately 19,056 hours over a five-month period.

Also based on extensive review, I conclude that Ocwen did not fail any of the compliance metrics tested during the first half of 2015 and continues to work on corrective action plans designed to fix past fails.

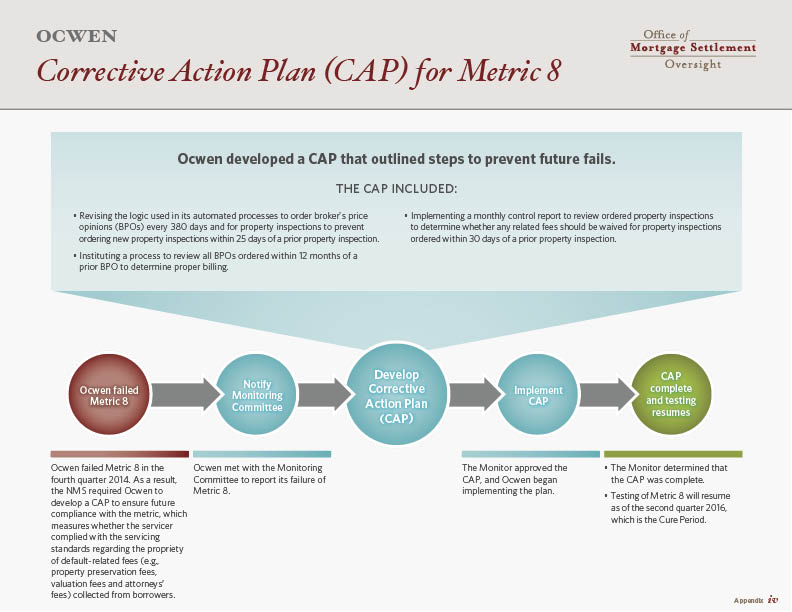

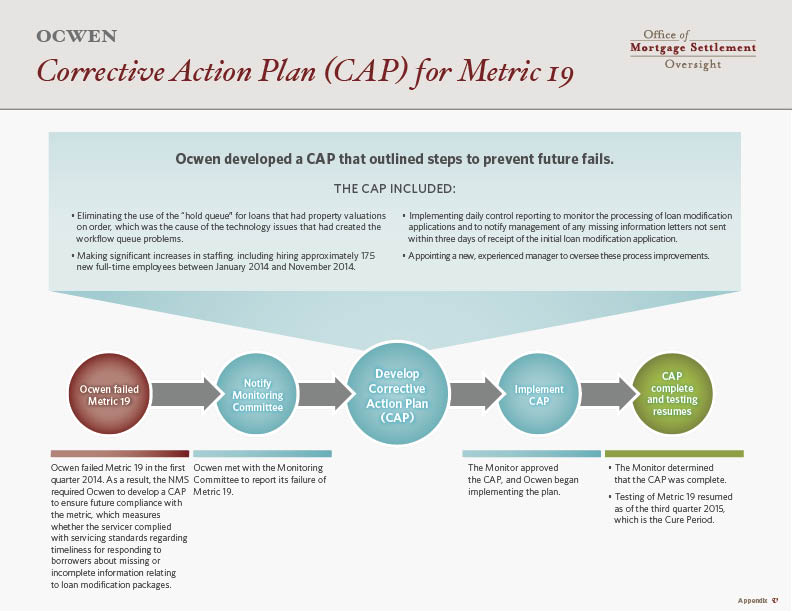

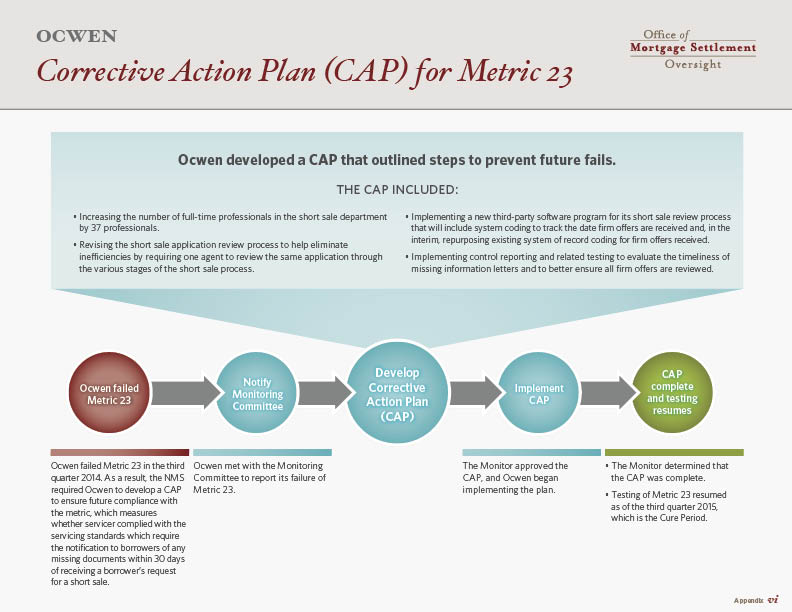

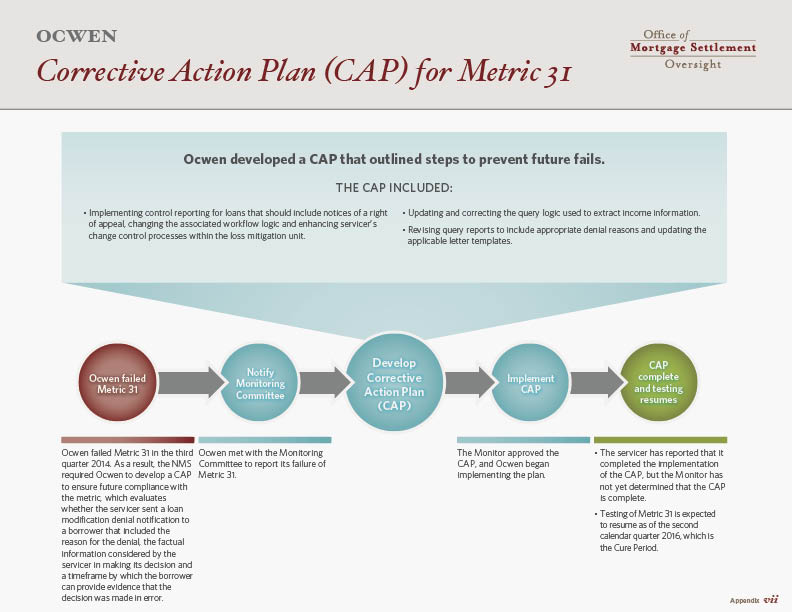

In October 2015, I reported that Ocwen failed four metrics in the second half of 2014.2 In addition, I deemed several metrics with timeline requirements also to be failures during that time as part of Ocwen’s Global Corrective Action Plan (Global CAP) to address its incorrect dating of borrower correspondence. As of the first quarter of 2015, there were ten metrics under a corrective action plan (CAP), the Global CAP or both. In this report, I provide updates on the current status of Ocwen’s cure efforts for the remaining metrics under CAPs, specifically Metrics 7, 8, 19, 23 and 31, as well as the Global CAP.

I am committed to making sure Ocwen correctly implements its plans to fix the issues that caused these failures and to remediate potential harm done to borrowers. I will continue reporting to the Court and the public on its progress.

Sincerely,

Joseph A. Smith, Jr.

Consumer Relief Testing and Results

Under the NMS, Ocwen Financial Corporation and Ocwen Loan Servicing, LLC (collectively, Ocwen) is required to provide $2 billion in consumer relief by February 26, 2017.

In August, I credited Ocwen with $881,219,183 toward its consumer relief obligation for certain activities completed through December 31, 2014. Ocwen’s IRG subsequently reported consumer relief credit of $1,246,478,441 for additional activities completed through September 30, 2015. My Primary Professional Firm (PPF), BDO Consulting, a division of BDO USA, LLP, reviewed the IRG’s assertion. After completing loan-level testing, my professionals determined that Ocwen’s IRG validated the consumer relief amounts and that Ocwen is entitled to consumer relief credit of $1,246,442,217 toward its consumer relief obligation. In total, I have credited Ocwen with $2,127,661,401 and have determined that Ocwen has exceeded its $2 billion consumer relief obligation.3

Non-Creditable Requirements

In addition to its consumer relief activities, Ocwen is required to meet certain noncreditable requirements under the Settlement. These non-creditable requirements require that the servicer’s policies not disfavor borrowers in any specific geograph or discriminate against any protected class of borrowers. In addition, servicers must not require a borrower to waive or release legal claims as a condition of approval for relief and may not receive any consumer relief credit for federal or state incentive payments Ocwen received for modifications made under federal or proprietary programs.

I conducted additional due diligence procedures to assure Ocwen is complying with these non-creditable requirements of the Settlement. Those procedures, in conjunction with the loan-level testing described earlier in this report, lead me to conclude that I have no reason to believe that Ocwen has not met the policy and procedure requirements outlined in the Settlement.

State Reports

Under the Settlement, I am required to identify any material inaccuracies in the State Reports that Ocwen files. As part of my review, I have undertaken procedures to identify any such material inaccuracies. Based upon the results of those procedures, I have determined that Ocwen’s States Reports did not contain any material inaccuracies.

Compliance Results

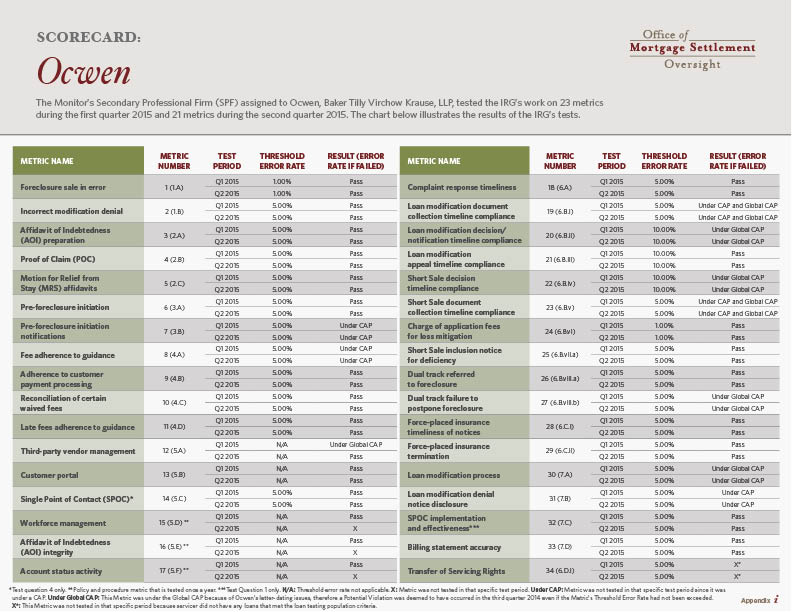

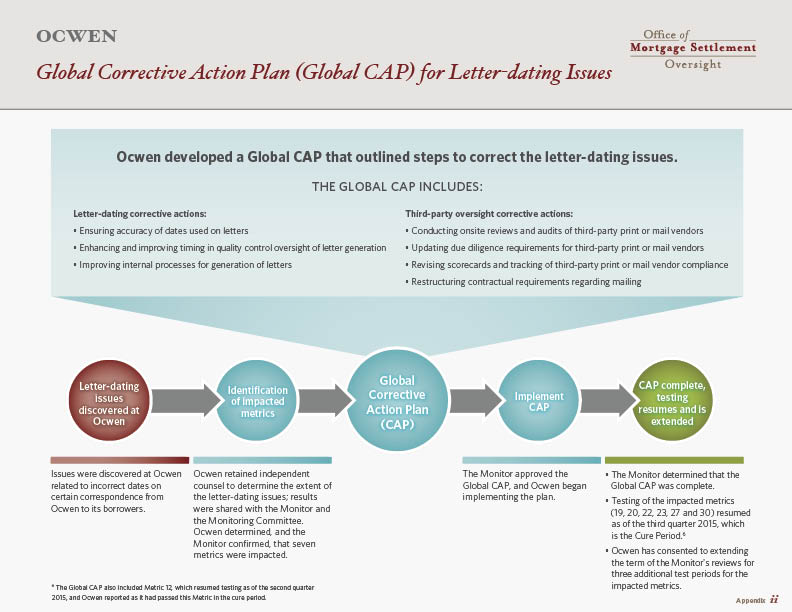

During the first and second quarters 2015, Ocwen did not fail any of the metrics tested. In October 2015, I reported that Ocwen failed Metrics 7, 23 and 31 in the third quarter 2014 and Metric 8 in the fourth quarter 2014. Additionally, Ocwen and I agreed that seven metrics (Metrics 12, 19, 20, 22, 23, 27 and 30) would be deemed failures due to Ocwen’s letter-dating issues.4 I outlined Ocwen’s Global CAP to address these issues in my previous report.

Below are updates on Ocwen’s progress in implementing CAPs and the Global CAP to address these fails.5

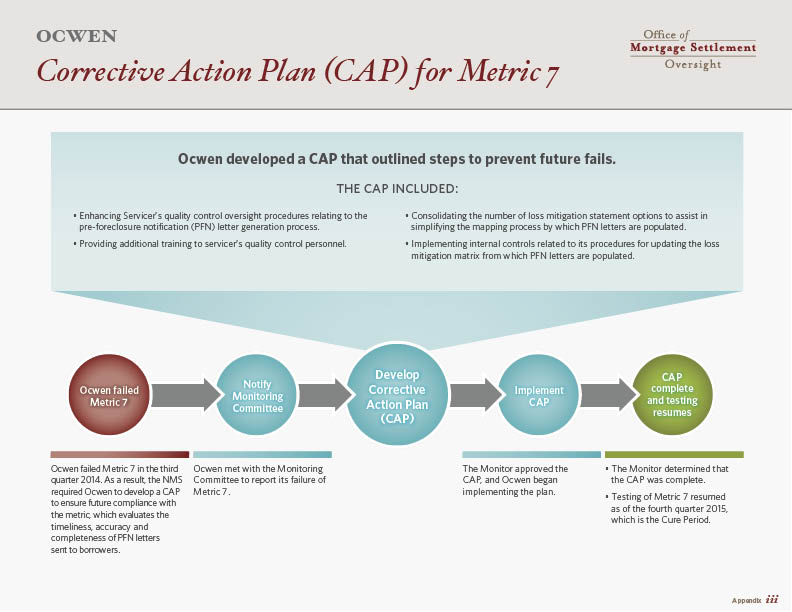

Metric 7 evaluates the timeliness, accuracy and completeness of pre-foreclosure initiation notification (PFN) letters sent to borrowers. After my reviews, I determined that the CAP for Metric 7 is complete, and testing resumed as of the fourth quarter 2015. I will report on whether the Metric 7 fail has been cured in my next report.

Metric 8 tests whether the servicer complied with servicing standards regarding the propriety of default-related fees (e.g., property preservation fees, valuation fees and attorneys’ fees) collected from borrowers. After my reviews, I determined that the CAP for Metric 8 is complete, and testing will resume as of the second quarter 2016.

Metric 19 tests whether the servicer complied with servicing standards regarding timeliness for responding to borrowers about missing or incomplete information relating to loan modification packages. I previously reported that the CAP was complete for Metric 19 and testing would resume as of the third quarter 2015. I will report on whether the Metric 19 fail has been cured in my next report.

Metric 23 tests the servicer’s compliance with the requirement to notify borrowers of any missing documents within 30 days of receiving a borrower’s request for a short sale. After my reviews, I determined that the CAP for Metric 23 is complete, and testing resumed as of the third quarter 2015. I will report on whether the Metric 23 fail has been cured in my next report.

Metric 31 tests whether the servicer sent a loan modification denial notification to a borrower that included the reason for the denial, the factual information considered by the servicer in making its decision and a timeframe by which the borrower can provide evidence that the decision was made in error. Ocwen has encountered delays in completing the implementation of the CAP. Ocwen’s delays appears to be related to difficulties in resolving certain technical issues that originally led to this metric failure. As a result, Ocwen submitted and I approved a revised Metric 31 CAP to address the cause of the technical issues. Ocwen recently informed me that the implementation of its Metric 31 CAP is now complete. If I determine that the CAP has been implemented, Ocwen expects testing to resume as of the second quarter 2016.

Ocwen notified me in October 2015 that it completed the Global CAP and concluded that the corrective actions were effective in remedying the letter-dating issues. After my reviews, I determined that the Global CAP is complete. Testing of the Global CAP metrics (19, 20, 22, 23, 27 and 30) will resume as of the third quarter 2015.6 I will report on whether these deemed fails due to the letter-dating issues have been cured in my next report.

Conclusion

Ocwen has satisfied its consumer relief obligation under the Settlement. In total, Ocwen has provided $2.1 billion in consumer relief and helped 23,802 borrowers through First Lien Mortgage Modifications. I am committed to making sure Ocwen continues its compliance with servicing standards under the Settlement through metrics testing. I am also working to ensure that these corrective actions work and testing resumes on all metrics as soon as possible. I will continue to report my findings on Ocwen’s compliance to the Court and the public.

Ocwen Consumer Relief Court Report

Court Report Regarding Potential Metric 19 Violation

1 The Court separately entered a consent judgment between Ocwen and government parties on February 26, 2014, as part of the NMS, thereby subjecting Ocwen’s entire portfolio to the Settlement’s requirements. Accordingly, beginning the third quarter 2014, Ocwen’s entire portfolio is subject to the Settlement’s requirements.

2 Ocwen failed Metrics 7, 23 and 31 in the third quarter 2014 and Metric 8 in the fourth quarter 2014.

3 Through its review process, the PPF determined that there was a duplicate loan included within the IRG Assertion for the Second Testing Period. The IRG subsequently confirmed the same. Thus, it was concluded that the servicer was entitled to claim credit in the amount of $1,246,442,217 through 14,941 First Lien Mortgage Modifications and that the total claimed credit reported as of September 30, 2015, is $2,127,661,401, through 23,802 First Lien Mortgage Modifications.

4 As detailed in my previous reports, the fails stemming from letter-dating issues were deemed to have occurred in the third quarter 2014. While considered a fail for purposes of addressing the letter-dating issues, Metric 19 was previously identified as a fail in the first quarter 2014 for reasons unrelated to the letter-dating issues and was already under a CAP as of the third quarter 2014. Metric 23 also exceeded the threshold error rate allowed under the settlement in the third quarter 2014 for reasons unrelated to the letter-dating issues.

5 Testing resumed for Metric 12 as of the second quarter 2015. Ocwen reported, and I confirmed, that Ocwen passed Metric 12 during the cure period.