Introduction

I am pleased to present my first report as Monitor under the Chase RMBS Settlement. This report’s purpose is to inform the public on the settlement’s requirements and provide an update on steps taken to date to implement the settlement. To those ends, the report includes:

- A summary of the terms of the agreements that comprise the settlement;

- A review of actions that have been or will be taken to implement the settlement;

- An overview of my responsibilities as Monitor of the settlement; and

- The results of my validation of Consumer Relief credit claimed as of March 31, 2014.

The Chase RMBS Settlement

On or about November 19, 2013, the United States Department of Justice (Justice) and a number of other governments and agencies of government (collectively, Government Parties) entered into five agreements with JPMorgan Chase & Co. (Chase) settling federal and state civil claims arising out of the packaging, marketing, sale and issuance of residential mortgage-backed securities by Chase, The Bear Stearns Companies, Inc. (Bear Stearns) and Washington Mutual Bank (Washington Mutual) prior to January 1, 2009. Together, these agreements are referred to as the Chase RMBS Settlement (Chase RMBS Settlement). The Chase RMBS Settlement was documented by:

- An agreement between Justice, the States of California, Delaware and Illinois, the Commonwealth of Massachusetts and Chase (Settlement Agreement); and

- Separate agreements (collectively, Separate Agreements) between Chase, Bear Stearns and, in all but one agreement, Washington Mutual and the State of New York, the Federal Housing Finance Agency (FHFA), the National Credit Union Administration (NCUA) Board, and the Federal Deposit Insurance Corporation (FDIC).

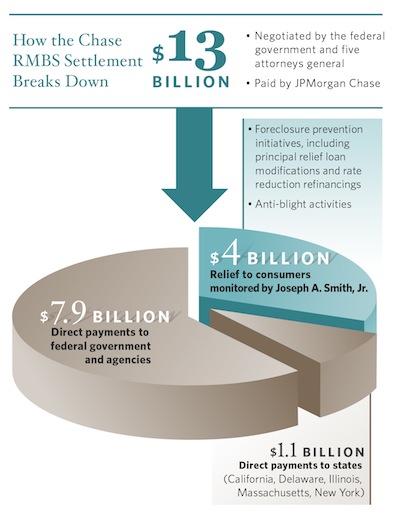

The Chase RMBS Settlement requires, among other things, that Chase make payments, aggregating $9 billion, to the Government Parties under the Settlement Agreement and Separate Agreements (Government Payments); and provide $4 billion of consumer relief to remediate harms allegedly resulting from unlawful conduct of Chase, Bear Stearns and Washington Mutual (Consumer Relief).

How the Chase RMBS Settlement Breaks Down

The Chase RMBS Settlement creates a position of independent Monitor to determine whether Chase has satisfied its Consumer Relief obligations. The parties to the Chase RMBS Settlement agreed that I, Joseph A. Smith Jr., would serve as Monitor.

The Government Payments

The Chase RMBS Settlement terms requires Chase to pay to:

- Justice:

- $2,000,000,000 to settle Financial Institutions Reform, Recovery, and Enforcement Act (FIRREA) claims

- $1,417,525,773 to settle NCUA claims

- $515,463,918 to settle FDIC claims

- Fannie Mae and Freddie Mac: $4,000,000,000 to settle claims pursuant to the FHFA’s Separate Agreement

- California: $298,973,006

- Delaware: $19,725,255

- Illinois: $100,911,813

- To Massachusetts: $34,400,000

- To New York: $613,000,235

Payment of the foregoing settlement amounts is not subject to oversight or review by the Monitor.

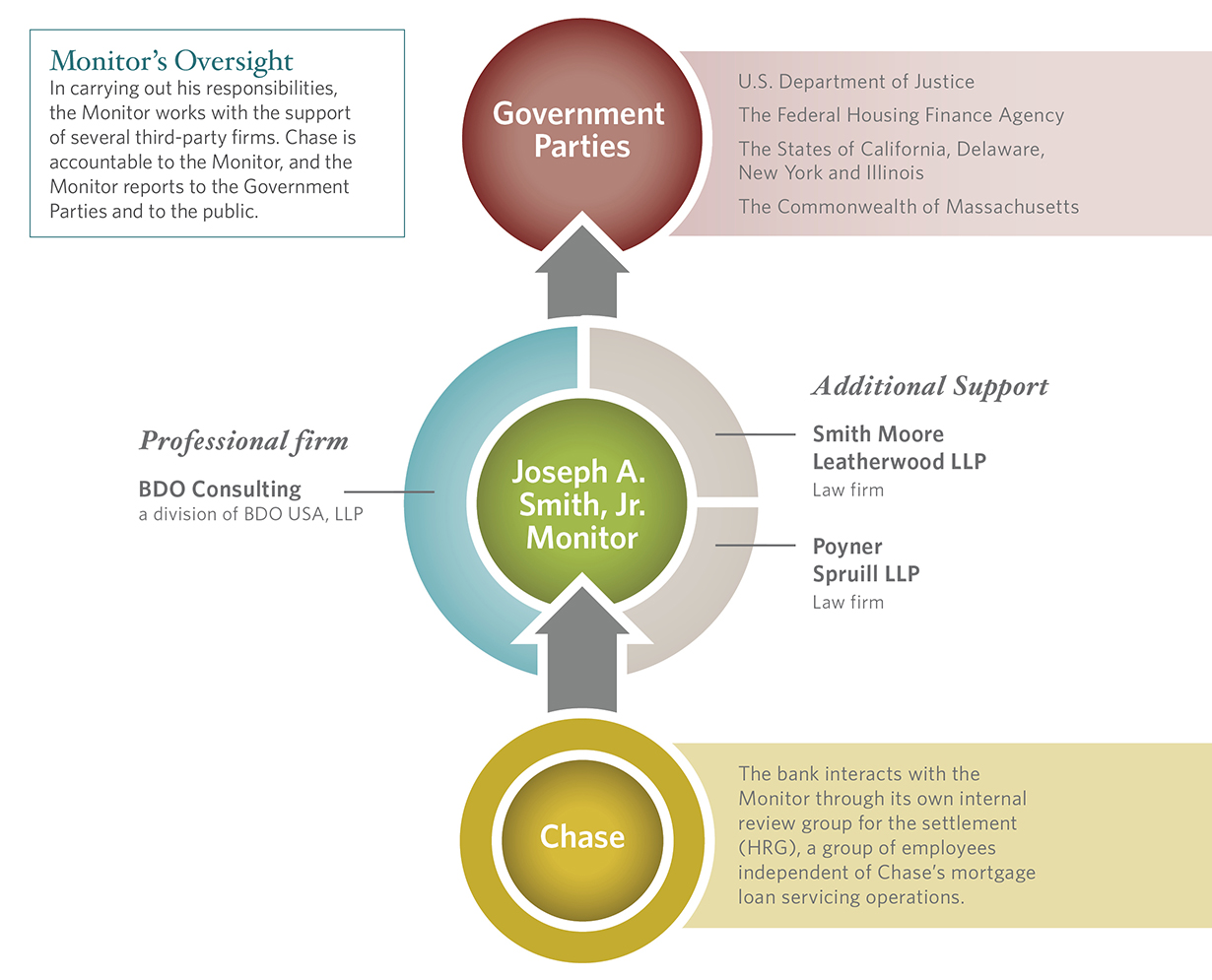

The Monitor and Professionals

As Monitor under the Chase RMBS Settlement, I am to determine whether Chase has satisfied its Consumer Relief obligations. To assist in this work, I have retained BDO Consulting, a division of BDO USA, LLP (BDO); Poyner Spruill LLP (Poyner Spruill); and Smith Moore Leatherwood LLP (Smith Moore and, together with BDO and Poyner Spruill, Professionals). I have confirmed that none of these Professionals have meaningful conflicts that would interfere with the integrity of our work.

Monitor’s Oversight

Consumer Relief under the Chase RMBS Settlement

Under the Settlement, Chase is required to provide $4 billion of Consumer Relief to distressed borrowers within essentially a four-year period, commencing October 1, 2013 and ending December 31, 2017.

Forms of Consumer Relief

Annex 2 to the Chase RMBS Settlement (Annex 2) defines various forms of Consumer Relief for which Chase can receive credit.

Modification – Forgiveness/Forbearance of First and Second Lien Mortgages:

- Eligible activities for credit in this category include first lien principal forgiveness, principal forgiveness of forbearance, first lien forbearance (payment forgiveness) and second lien principal forgiveness modifications (including extinguishments).

- Credit may only be given for loans as to which relief was completed on or after October 1, 2013.

- No credit may be given for a loan modification requiring payments unless the borrower makes the first three scheduled payments under the modification (including trial payments).

- Credit for principal forgiveness modifications must be net of any state or federal payments made to Chase in respect of such forgiveness.

- All first lien principal forgiveness and forgiveness of forbearance relief must be with respect to loans with an unpaid principal balance prior to capitalization at or below the highest national GSE conforming loan limit cap as of January 1, 2010.1

Rate Reduction/Refinancing:

- Credit may be given for rate reductions or refinancings.

- Credit for refinancing includes cross-servicer refinancing through HARP.

Low to Moderate Income, Disaster Area, and Other Lending:

- Credit is available for purchase money loans to creditworthy borrowers who:

- are in locations identified by the United States Department of Housing and Urban Development (HUD) as hardest hit areas,

- are in areas declared as Major Disasters by FEMA between Oct. 1, 2012 and Nov. 19, 2013,

- lost homes to foreclosure or short sales, or

- are first time low to moderate income (LMI) homebuyers.

Anti-Blight:

- Credit is available for:

- forgiveness of principal where foreclosure is not pursued,

- cash costs for demolition of dilapidated properties,

- donated mortgages or REO properties to certain parties, and

- funds donated to capitalize community equity restoration funds or similar community redevelopment activities.

Eligibility

As reflected in Annex 2 and summarized above, each of the forms of Consumer Relief has unique eligibility criteria. In order for Chase to receive credit with respect to Consumer Relief activities on any mortgage loan, these eligibility criteria must be satisfied with respect to such mortgage loan and such satisfaction has to be validated by me in accordance with paragraph 2 of the Settlement Agreement and Annex 2.

Credit Amounts

Chase will receive different amounts of credit depending upon the type of Consumer Relief activity performed and the ownership of the affected loan. For first and second lien principal forgiveness, Chase will receive one dollar of credit for each dollar forgiven on the eligible loans it holds for investment. For each dollar of principal forgiven on loans that are serviced for others, Chase will receive 50 cents of credit. For second lien loans that are greater than 90 days past due, Chase will receive 40 percent of the credit it otherwise would have received.

For rate reductions and refinancings, Chase will receive credit based on formulas involving the amount of the rate reduction, average life of the loan,2 and the unpaid principal balance of the loan.3 For forbearance on first liens, the crediting formula includes the pre-modification interest rate, the average life of the loan, and the forborne unpaid principal balance. In both instances (rate reduction/refinancing and first lien forbearance), the credit for loans serviced for others is 50 percent of the credit for loans held for investment.

Chase will receive $10,000 in credit for each purchase money loan to eligible credit worthy borrowers in the low to moderate income, disaster area and other lending category. Finally, for its anti-blight relief, Chase will receive one dollar of credit for each dollar of write down, payment, or property value, depending upon the specific activity.

Bonuses and Penalties

The Chase RMBS Settlement provides bonus credits of 25 percent for any first or second lien modifications, refinancing or rate reduction transactions, or LMI/disaster area lending in hardest hit areas. The settlement also provides an early incentive bonus credit of 15 percent for the foregoing Consumer Relief transactions completed before October 1, 2014. This early incentive credit and the bonus credit for hardest hit areas are cumulative. It also provides that if I determine that Chase has not satisfied its Consumer Relief obligations by December 31, 2017, then Chase must pay the shortfall to NeighborWorks America as liquidated damages.

Minimums and Caps

Chase has discretion as to the provision of the kinds of Consumer Relief described above to meet its overall obligations, subject to minimums and caps on certain types of relief. Of the $4 billion of Consumer Relief credit, at least $2 billion must be first or second lien principal forgiveness, principal forgiveness of forbearance, or first lien forbearance (payment forgiveness), and at least $1.2 billion must be principal forgiveness of first liens or forbearance. That said, there is a $300 million cap on credit for principal forgiveness of forbearance and an additional cap of $300 million on credit for first lien forbearance (payment forgiveness). Finally, there is a cap of $165 million on credit for lending in disaster areas.

Principles and Conditions

The Chase RMBS Settlement also provides for several principles and conditions relating to Consumer Relief, including that:

- Relief will not be implemented through any policy that violates the Fair Housing Act or the Equal Credit Opportunity Act;

- Relief will not be conditioned on a waiver or release of legal claims and defenses as a condition of approval for loss mitigation, except in cases of a contested claim where the borrower would not receive as favorable terms or consideration; and

- Eligible modifications may be made under the Making Home Affordable Program, including HAMP, and the Housing Finance Agency Hardest Hit Fund, and any proprietary or other modification program.

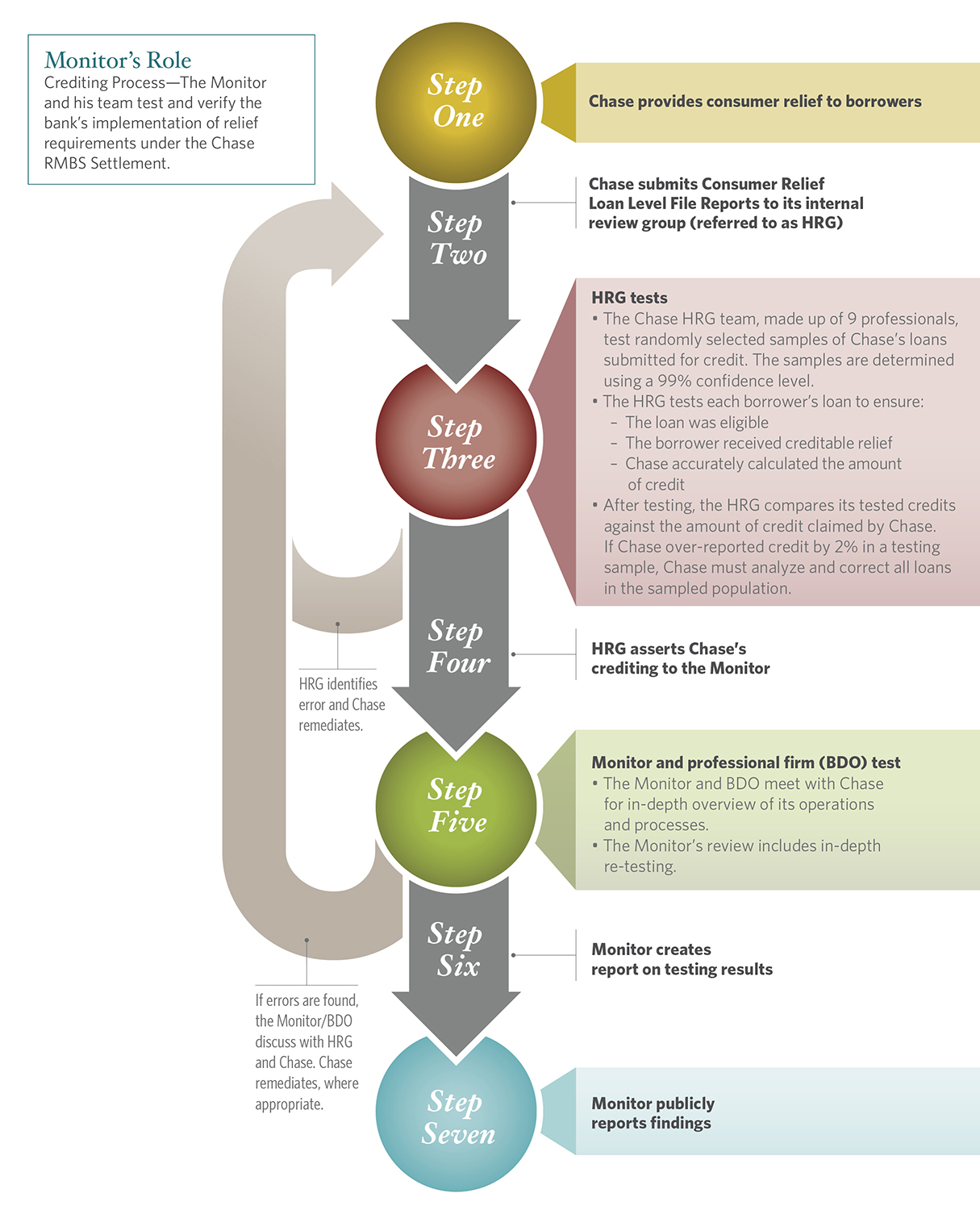

Reporting, Testing and Assertion of Relief

Relief crediting requires the following actions by three distinct entities:

- Chase will perform the Consumer Relief activities and report to me quarterly. For testing and validation, it will also report its activities via a Consumer Relief Loan Level File Report to an internal review group (HRG4), a group of employees independent of Chase’s mortgage loan servicing operations.

- The HRG will test and confirm the eligibility of Chase’s Consumer Relief activities and the amount of credited relief through satisfaction reviews at appropriate times (“Satisfaction Reviews”), and report to me the results of each Satisfaction Review through an HRG Assertion5; and

- As Monitor, I will determine whether and when Chase has satisfied its obligations. I will work with BDO and, as necessary, the other Professionals to review the HRG’s Satisfaction Reviews and conduct other procedures as I deem appropriate to determine whether the HRG Assertion is correct and complete.

In doing this work, the HRG, Professionals and I will use methods outlined in an agreed-upon work plan and definitional templates to determine that all or a portion of Chase’s Consumer Relief obligations have been performed or satisfied.

Crediting Process

My Reporting Obligations

The Chase RMBS Settlement terms require that I publicly report on the following:

- Progress towards completion, including reporting on overall progress, on a quarterly basis commencing no later than 180 days after the date of the Settlement Agreement;

- Credits earned as promptly as practicable following the date I have validated the credits; and

- Final certification of Chase’s compliance with its Consumer Relief obligations, as appropriate.

Progress to Date

In the months since the parties selected me, my Professionals and I have met and conferred with Justice and Chase on multiple occasions to establish the framework described above. My Professionals and I negotiated with Chase a work plan and related definitional templates under which the HRG’s work and my review and assessment of Consumer Relief are being conducted.

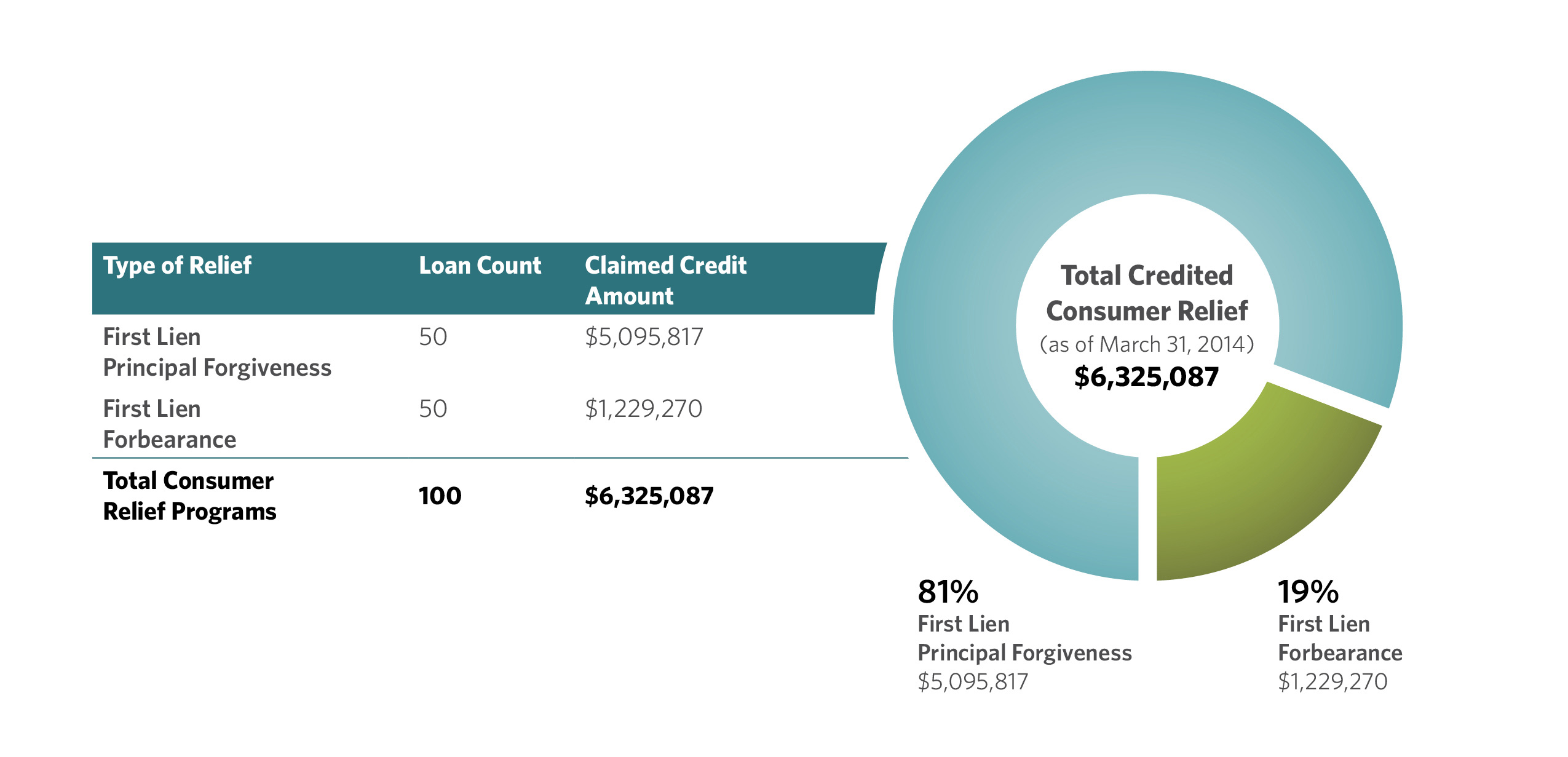

On May 15, 2014, after completing a Satisfaction Review, the HRG submitted to me an HRG Assertion regarding the amount of Consumer Relief credit that Chase claimed to have earned as of March 31, 2014 in relation to 100 loans. According to the HRG Assertion, as of March 31, 2014 Chase has correctly claimed $6,325,087 of Consumer Relief credit, pursuant to Annex 2, for first lien principal forgiveness and first lien forbearance on those loans.

Prior to the submission to me of the HRG Assertion, Chase informed me that it intended to submit for review 100 first lien modifications to the HRG for the period ending March 31, 2014. Chase indicated that it elected to take this approach so that the HRG could use this initial testing period to ensure that its testing protocols were appropriately designed. Chase further advised me that, as of March 31, 2014, it had provided creditable relief to borrowers on other loans that were not included in the group of 100 loans tested by the HRG in issuing the May 15, 2014 HRG Assertion and that it intends to submit those other loans to the HRG for validation at a later date. I consented to the approach taken by Chase.

Approximately 56 percent of the credit was a result of relief afforded to borrowers on loans in Chase’s mortgage loan portfolio that is held for investment; and the remainder was a result of relief afforded to borrowers on loans that Chase was servicing for others. Approximately 81 percent of Chase’s claimed credit was through first lien principal forgiveness and approximately 19 percent was through first lien forbearance. The table immediately below sets out a breakdown of the Consumer Relief credit, by type of relief, as set forth in the May 15, 2014 HRG Assertion:

Credited Consumer Relief

Chase has requested that, in addition to reporting on the HRG Assertion, I review the 100 loans and validate that the amount of credit claimed in the HRG Assertion is accurate and in accordance with Annex 2.

HRG’s Satisfaction Review

After submitting its initial HRG Assertion on May 15, 2014, the HRG reported to me the results of its Satisfaction Review, which report concluded that:

- the Consumer Relief asserted by Chase for the testing period was based upon completed transactions that were correctly reported by Chase;

- Chase had correctly credited such Consumer Relief activities, so that the claimed amount of credit is correct; and

- the claimed Consumer Relief correctly reflected the requirements, conditions and limitations, as currently applicable, set forth in Annex 2.

To reach the conclusions set forth above, the HRG conducted an independent review to determine whether each of the 100 loans was eligible for credit and the amount of credit reported by Chase was calculated correctly.6 The HRG executed this review pursuant to and in accordance with the work plan and definitional templates, as well as test plans it has created,7 by accessing from Chase’s system of record8 (SOR) the various data inputs required to undertake the eligibility determination and credit calculation for each loan. Additionally, the HRG captured and saved in its work papers available screenshots from Chase’s SOR evidencing the relevant data. For each loan, the HRG determined whether it was eligible for credit based upon the assembled data for that loan, again following the appropriate definitional template and related test plans. If a loan was determined to be ineligible for credit, the HRG would conclude that Chase should receive no credit for that loan. For each loan it determined to be eligible for credit, the HRG would recalculate the credit amount.

After verifying the eligibility and recalculating credits for the 100 loans Chase submitted for credit, the

HRG calculated the sum of the recalculated credits for the Testing Population (Actual Credit Amount) and compared that amount against the amount of credit claimed by Chase for the 100 loans in the Testing Population (Reported Credit Amount). According to the work plan, if the Actual Credit Amount equals the Reported Credit Amount or if the Reported Credit Amount is not more than 2.0 percent greater or less than the Actual Credit Amount, the Reported Credit Amount will be deemed correct and Chase’s Consumer Relief Report will be deemed to have passed the Satisfaction Review and will be certified by the HRG to me. If, however, the HRG determined that the Reported Credit Amount exceeded the Actual Credit Amount by more than 2.0 percent, the HRG would inform Chase, which would then be required to perform an analysis of the data of all loans in the Testing Population, identify and correct any errors and provide an updated Consumer Relief Loan Level File Report to the HRG. The HRG would then test the Testing Population against the updated report in accordance with the process set forth above. If the HRG determined that the Actual Credit Amount was greater than the Reported Credit Amount by more than 2.0 percent, Chase had the option of either (i) taking credit for the amount it initially reported to the HRG or (ii) correcting any underreporting of Consumer Relief credit and resubmitting loans to the HRG for further testing in accordance with the process set forth above. Utilizing the steps set forth above, the HRG determined that the Reported Credit Amount did not exceed the Actual Credit Amount by more than the 2.0 percent error threshold described above.9 These findings by Testing Population are summarized in Table 2, below:

Table 2

Based upon the results set forth above, the HRG certified that the amount of Consumer Relief credit claimed by Chase in the Testing Population was accurate and conformed to the requirements in Annex 2. This certification was evidenced in the HRG Assertion in the form required by the work plan.

Monitor’s Review

Preliminary to my review of the results of the HRG’s Satisfaction Review, I, along with some of my Professionals, met with representatives of Chase to gain an understanding of its mortgage banking operations, SOR and HRG program, and the HRG’s proposed approach for Consumer Relief testing, among other things. During those meetings, Chase provided an overview and walkthrough of its SOR and described its relevant core processing application for mortgage loans (Mortgage Servicing Platform), core processing application for home equity loans (Vendor Loan System), application used to modify loans (Agent Desktop), core processing application for default home equity loans (Recovery One) and the internet and intranet web portal application for digital document access and retrieval for default loans across enterprise document archives (LenderLive). Chase also provided me, together with the Professionals, with an overview of the HRG program, the personnel assigned to the HRG, and the HRG’s training approach, team management and internal controls designed to ensure the HRG’s work papers appropriately document and support the conclusions of the HRG’s work. Additionally, they described the testing approach the HRG planned to employ to, among other things, evaluate the eligibility of the loans for which credit is claimed and verify the accuracy of the credit calculation.

At my direction, BDO conducted an extensive review of the testing conducted by the HRG relative to Consumer Relief crediting. The review of Consumer Relief crediting began in May 2014, and continued, with only minimal interruption, until the filing of this report.

The principal focus of the review was BDO’s testing of the 100 loans tested by the HRG, following the processes and procedures set out in the work plan and applicable definitional template. This review also included, among other due diligence: (i) in-person walkthrough on May 21, 2014 at the HRG’s location in Columbus, Ohio of the HRG’s approach to test the two types of consumer relief that were reported in the May 15, 2014 HRG Assertion and (ii) numerous email and telephonic communications between BDO and the HRG during which BDO requested additional evidence and made inquiries concerning the HRG’s testing methodologies and results.

With respect to BDO’s testing, BDO was afforded access to a list of and accompanying detail for the 100 loans for which credit was claimed by Chase and tested by the HRG and provided remote access via Chase’s secure Citrix platform during its review and testing of those loans. Additionally, for each loan that it had tested, the HRG provided the data elements and evidence necessary for validating credits in accordance with Annex 2 and the applicable definitional template. BDO, using the data elements and evidence, went through each of the test steps and related analyses and calculations in the definitional template for each of the 100 mortgage loans. In other words, BDO replicated in full the HRG’s testing. During this process, the HRG cooperated fully with BDO.

After completing the loan-level testing, BDO determined that the HRG had correctly validated the Consumer Relief credit amount reported by Chase. The results of BDO’s loan-level testing are set forth in Table 3, below:

Table 3

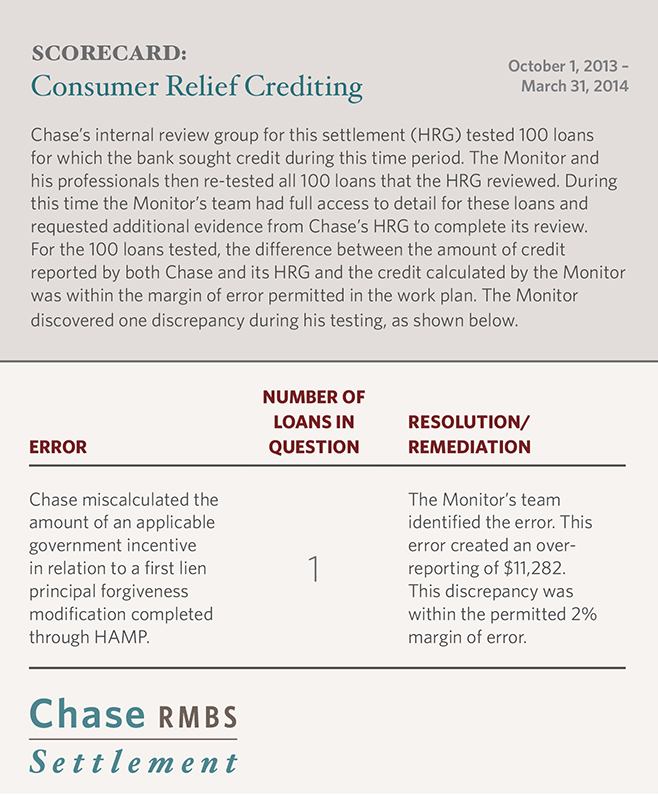

Consumer Relief Crediting Scorecard

For the 100 loans tested, the difference between the Reported Credit Amount and the credit amount as calculated by BDO was within the margin of error in the work plan. In addition, other than BDO finding an isolated instance of Chase and the HRG overstating the amount of credit earned in relation to a first lien principal forgiveness modification completed pursuant HAMP because they had miscalculated the amount of an applicable government incentive, BDO’s credit calculations and the HRG’s credit calculations were the same.

BDO documented its findings in its work papers and has reported them to me. I then undertook an in-depth review of the HRG’s work papers with BDO, as well as BDO’s work papers.

Summary and Conclusions

On the basis of the information submitted to me and the work as described in this Report, I report the following:

- I have determined that the amount of Consumer Relief set out in Chase’s Consumer Relief Loan Level File Report for the period extending from October 1, 2013, through March 31, 2014, is correct and accurate within the tolerances permitted under the Work Plan; and

- I have no reason to believe that Chase has failed to comply with all of the requirements of Annex 2 to the Settlement for the period extending from October 1, 2013, through March 31, 2014.

My next report to the public on Chase’s consumer relief activity will be issued before the end of the year.

1 GSE conforming loan limit caps as of January 1, 2010 are: 1 Unit, $729,750; 2 Units, $934,200; 3 Units, $1,129,250; and 4 Units, $1,403,400.

2 The average life of the loan is based upon eight years for eligible (1) refinancings in which the modified term is for the life of the loan and (2) cross-servicer refinancings conducted pursuant to the Home Affordable Relief Program (HARP); for all other eligible refinancings, the average life of the loan is based upon five years.

3 For forgiveness of forbearance, the average life of the loan is based upon eight years.

4 The HRG is distinct from the IRG, the internal review group in the National Mortgage Settlement.

5 The HRG Assertion is a certification given to me by the HRG regarding the credit amounts reported in Chase’s Consumer Relief Loan Level File Report.

6 According to the work plan, the HRG is to test a statistically valid sample from each of four different testing populations, which are (1) Modification – Forgiveness/Forbearance; (2) Rate Reduction/Refinancing; (3) Low to Moderate Income and Disaster Area Lending; and (4) Anti-Blight. In determining the sample size, the work plan requires that the HRG utilize a 99% confidence level (one tailed), 2.5% estimated error rate and 2% margin of error approach (99/2.5/2 approach). Because the Consumer Relief Loan Level File Report that was the subject of the Satisfaction Review resulting in the May 15, 2014 HRG Assertion contained only 100 loans, all of which were in the Modification – Forgiveness/Forbearance testing population, the HRG tested all of the loans in that one testing population.

7 The test plans are developed by the HRG based upon the definitional templates. They are tailored to Chase’s System of Record and business practices in the areas of mortgage loan servicing and offer a step-by-step approach to testing mortgage loans in each of the different types of Consumer Relief. These test plans set out “click by click” processes and procedures that reviewers have to undertake to access and review a number of both interrelated and separate electronic and other data systems. As they are developed, these test plans are reviewed and commented upon by me and other Professionals engaged by me.

8 System of record or SOR means Chase’s business records pertaining primarily to its mortgage servicing operations and related business operations.

9 Because, in conducting the testing that resulted in the May 15, 2014 HRG Assertion, the HRG tested all of the loans in one testing population rather than a sample of those loans as contemplated by the work plan, had the Reported Credit Amount exceeded or was less than the Actual Credit Amount by more than 2%, the appropriate remedy would have been to adjust the amount of credit that Chase claimed as a result of the loans in that testing population to equal the Actual Credit Amount. Chase would not have to conduct any additional analysis of the loans in the Testing Population and additional testing would not be necessary since the HRG had tested all loans in the testing population.